The Move That Will Save You Money

Learn About the Move That Will Save You Money

No one wants to pay more to their insurance company than they have to. Your money is a precious resource and spending healthcare dollars wisely is a priority.

Learn about how you could be paying more than you have to for your Medicare Supplement plan and what you can do to save money every month on your Medicare Supplement plan premium.

Plan F Costs Are Going Up

Plan F has been the long-standing supplement plan favorite because it pays all medical costs after Medicare pays their share. Not receiving medical bills is great, but the monthly premiums for Plan F are getting higher and higher.

The premium increases for Plan F are expected to continue rising at a rate that outpaces other plans.

Many new Medicare beneficiaries started opting for Plan G instead of Plan F a couple of years ago, which has played a role in Plan F premium increases over the last two years.

An Act was passed by Congress in 2015 that closed Plan F enrollment to anyone entering Medicare for the first time after January 2020. The result of that rule is that the average age of Plan F members will increase every year going forward.

With no new, younger and presumably healthier people joining the risk pool, Plan F premiums will continue to go up at a faster rate than other plans.

You need to ask yourself if the money you're paying every month in premiums makes sense for the benefits that you get. Does the math add up?

What Can You Do To Save Money?

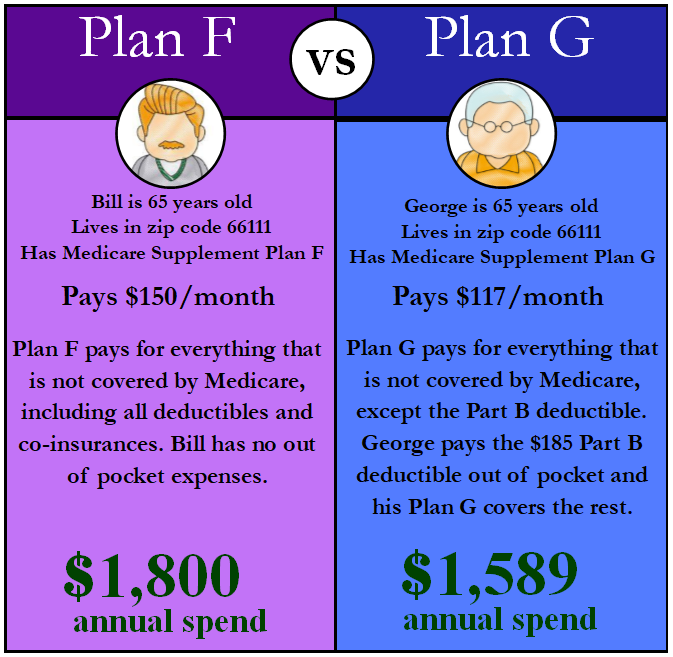

You're probably wondering what the difference between Plan F and Plan G is.

Well, it's not much! Take a look at the chart above. Plan F and Plan G cover all of the same services, except Plan G does not cover the Part B annual deductible, which is $185.

That means that at the beginning of each year, you will have to pay the first $185 of your Part B services. Once you have paid that amount, Plan G pays everything else, the same way Plan F does.

That $185 each year is pennies compared to the premium savings many people experience by dropping their Plan F and switching to Plan G!

Never cancel your current Medicare Supplement Plan until you have been approved for a new policy and that policy has been issued.

There are two things to love about Medicare Supplement plans:

1. You can change your supplement plan any time of the year without the worry of short enrollment periods, unlike the strict enrollment periods that apply when you turn age 65 or the annual enrollment period for Advantage and Part D drug plans.

2. Plans are standardized, which means that you know exactly what benefits you will get, regardless of the company you enroll with. For example, a Plan F with Humana is exactly the same as a Plan F with Aetna. The only difference is the company name on your card and how much you pay each month!

You can read more HERE from medicare.gov on how the plans are standardized.

What Do You Have To Do To Save?

There is one potential obstacle to face as a trade-off for having no enrollment period; your application for the new plan is subject to medical underwriting approval.

Medical underwriting approval means that the insurance company can approve or deny your application for enrollment based on your medical history over the past 2-5 years and your current medical conditions.

You don't have to go through a medical screening or physical. The insurance company is just looking for major health conditions like heart attack, stroke, cancer and Alzheimer's among other serious conditions. Additionally, each company has a list of certain medications they will not accept.

The application will ask you to answer 12-14 health questions, to provide a list of your medications and what doctors you've seen in the last couple of years. With that information, the insurance company decides to approve or deny your application.

Time is of the essence. If you're healthy and can be approved today, don't wait until an unforeseen medical issue comes up and you can't change your plan.

An unexpected medical event can make you uninsurable (unable to change) for up to five years.

You don't want to regret not changing when you could and then be stuck paying high premiums.

Happy to help.

We help clients save $100-$250 on their premiums every month by simply switching from Plan F to Plan G or changing the insurance company that provides the benefits for their current plan.

Earlier this month, we helped a couple in North Carolina save $180 on their monthly premiums by changing the insurance company that provided their Plan G benefits.

The only issue they had was that they did not agree on how they were going to spend the extra $2,160 they would have in the coming year. That's an issue we don't mind seeing!

We would be delighted to help you save money on your healthcare premiums while ensuring you have a quality plan that fits your needs.

Contact us today to see how much you could save, what premium discounts you qualify for and expert guidance to help you every step of the way!

Just in case you are a do-it-yourself type of person, we have a free quote tool on our website that you can use.

Click HERE to see the cost of plans in your area.

Note: Discounts you might qualify for won’t be reflected. Premiums could be 7-12% less than what you find.